Impact of Tripling of Capital Gains Tax on Property Sales in Kenya Effective January 1, 2023

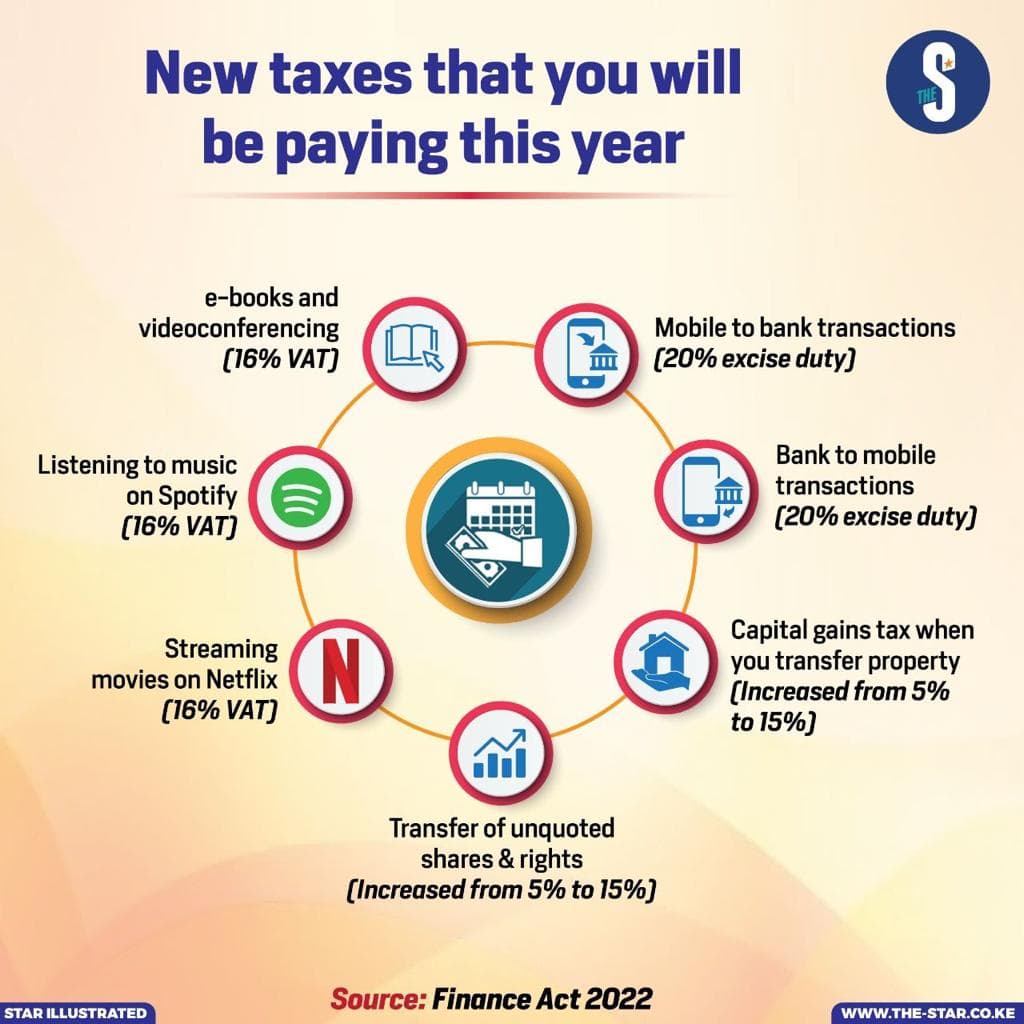

The Finance Act of 2022 amended the Income Tax Act, increasing the rate of capital gains tax, or CGT, from 5 percent to 15 percent (effective from January 1, 2023)

What is Capital Gains Tax (CGT)?

CGT is a tax imposed on the transfer of property situated in Kenya that was acquired on or after January 2015. It is declared and paid by the transferor of the property.

🏛️ Definition of Transfer of Property:

A transfer of property includes the exchange, conveyance, or other disposition of property, as well as the destruction, abandonment, surrender, cancellation, or forfeiture of property. Examples of properties that may incur CGT when transferred include land, buildings, securities, and shares.

CGT Rate Determination

The rate of Capital Gains Tax in Kenya is determined by the specific circumstances of the transfer. For example, a firm certified by the Nairobi International Financial Centre Authority that invests KES 5 billion in Kenya and transfers the investment after five years will be subject to the rate that was in effect at the time of the investment. This means that if the firm invested before the CGT rate was increased to 15 percent, it would still be subject to the lower rate of 5 percent when it makes the transfer.

Allowable Expenses to Compute CGT

How to Compute CGT

Calculation Formula:

Total Capital Gain - Allowable Expenses = Net Capital Gain

Net Capital Gain × Applicable Rate (15%) = CGT Liability

📊 Example:

If total capital gain on property transfer = KES 10,000,000

Allowable expenses = KES 2,000,000

Net capital gain = KES 8,000,000

CGT due (15%) = KES 1,200,000

How to Pay CGT in Kenya

- File a return with the Kenya Revenue Authority (KRA) within three months of the transfer

- Tax must be paid within 30 days of filing the return

CGT Exemptions

- Transfer of property to secure a loan

- Transfer of assets between spouses

- Transfer of shares listed on the Nairobi Securities Exchange

- Transfer of property by a creditor to return property used as security for a debt or loan

Expected Impact of CGT Increase

📚 Additional Resources

Check out Everything You Need To Know about Capital Gains Tax by KRA.

📋 Important Disclaimer

We hope this information helps understand the capital gains tax laws and computation in Kenya. Please note that the contents of this article are intended to provide a general guide to the subject matter. It should not be relied upon without legal and financial advice on its contents.

Need Legal Assistance?

Should you require further information or legal assistance on Compliance or any other legal matter, kindly feel free to contact:

William Karoki

WKA ADVOCATES

Nairobi Hub: Parklands, Valley View Business Park, 6th Floor

City Park Drive, Off Limuru Road

📋 CGT Quick Reference

🎯 Key Takeaways

- CGT rate increased from 5% to 15% effective January 1, 2023

- Applies to property acquired on or after January 2015

- Allowable expenses reduce taxable gain

- Exemptions available for certain transfers

- Higher CGT may slow real estate market activity

- Seek professional legal and tax advice for specific situations

House Hunting, Land Buying & Property Marketing

Smarter with Hao Finder™

Whether you're looking for your next home, investing in land, or marketing real estate listings — Hao Finder™ gives you verified properties, expert insights, and digital tools that simplify your journey.

Call us

+254 715 560 734

+254 118 582674

+973.253.3800

Email us

info@haofinder.com

business@haofinder.com

Location

Delta Corner Towers, Westlands, Nairobi |

471 Mundet Place, Ste. US159850 |

Hillside, New Jersey 07205,

United States